A non-government resource

Compare

Learn

About Us

Last Updated March 2026

Top Medicare Insurance Companies of 2026

Last Updated March 2026

Top Medicare Insurance Companies of 2026

Find the top health insurance coverage

Take the guesswork out of health insurance - we consolidate reviews so you don’t have to.

#1

Best customer experience

9.1

CoverRight

Free Medicare guidance and online rate comparison

Personalized recommendations

Instant quotes online from multiple top carriers

Offers Medicare Advantage and Medigap Plans

Direct access to a licensed agent - 100% free with no obligation to enroll

#2

7.9

UnitedHealthcare

Largest healthcare insurer and network of providers in the country

Largest Medicare Advantage network - more than 1 million providers

Partners with AARP for some plans

Member satisfaction lower than some other carriers in certain regions according to J.D Power

via CoverRight

#3

7.7

Humana

Provides high quality plans across the country

Available in 89% of U.S. counties and ‘A’ financial strength rating

Has select veteran-focused plans designed to work with veteran benefits

Member satisfaction tends to be below regional average according to J.D. Power

via Humana

#4

6.9

Aetna

Variety of plans and benefits available across the country

Broadly available - with offerings in 43 states and D.C.

Aetna is a CVS Health company so you can access the benefits of being with a CVS pharmacy

Fewer plans available overall than prior years

via CoverRight

#5

6.5

Blue Cross Blue Shield

Medicare Advantage plans available vary by state

Offers large number of affordable plans across the country

Overall good customer satisfaction

Coverage is dependent on state-based BCBS company that license the brand

via CoverRight

#6

5.6

Healthspring (formerly Cigna)

Large number of highly rated plans, though costs can be higher

Large number of strongly rated plans

Customer satisfaction results vary

Lower availability across the country than other carriers

via Healthspring (formerly Cigna)

visitors

found a Medicare

plan this week

Advertising Disclosures

The TopMedicare Score scoring system incorporates a weighted formula, which considers three parameters, providing a numerical score out of 10.

Trustpilot Score

Trustpilot is a third-party independent customer review platform. You can read more about Trustpilot by visiting their site here.

Click Score

The Click Score represents user engagement based on the number of clicks each company has received over the past 7 days. The number of clicks to each brand is measured against other brands listed in the same query. The higher the share of clicks a company receives, the higher the Click Score.

Review Score

The Review Score is based on TopMedicare’s team’s review of third party trusted and comprehensive sources. This is an overall score given by an weighted-average of the third-party publications based on their editorial teams research and review of each product, and includes factors such as service quality, ease-of-use, online availability and more.

Editorial Reviews

At TopMedicare, we consolidate third party review sources so you don’t have to:

CoverRight

Read Review

UnitedHealthcare

Read Review

Humana

Read Review

Aetna

Read Review

BCBS

Read Review

Healthspring

Read Review

Our Top Choice for Medicare Insurance in March 2026

Our top pick

9.1

CoverRight

Free Medicare guidance and online rate comparison

Personalized recommendations

Instant quotes online from multiple top carriers

Offers Medicare Advantage and Medigap Plans

Direct access to a licensed agent - 100% free with no obligation to enroll

Medicare 101: What is Medicare?

Understanding Medicare basics is critical to making sure you have the right health insurance.

What is Medicare?

Medicare is a federal program that provides health insurance to those over the age of 65, as well as certain individuals under 65 with disabilities.

The goal of Medicare is to provide health insurance coverage to eligible individuals (called ‘beneficiaries’) regardless of income, medical history, or health status. In 2026, Medicare covered over 62 million beneficiaries in the U.S. including 54 million aged 65 and older.

Medicare should not be confused with Medicaid, which is a federal and state program that helps with medical costs for those with limited income and resources.

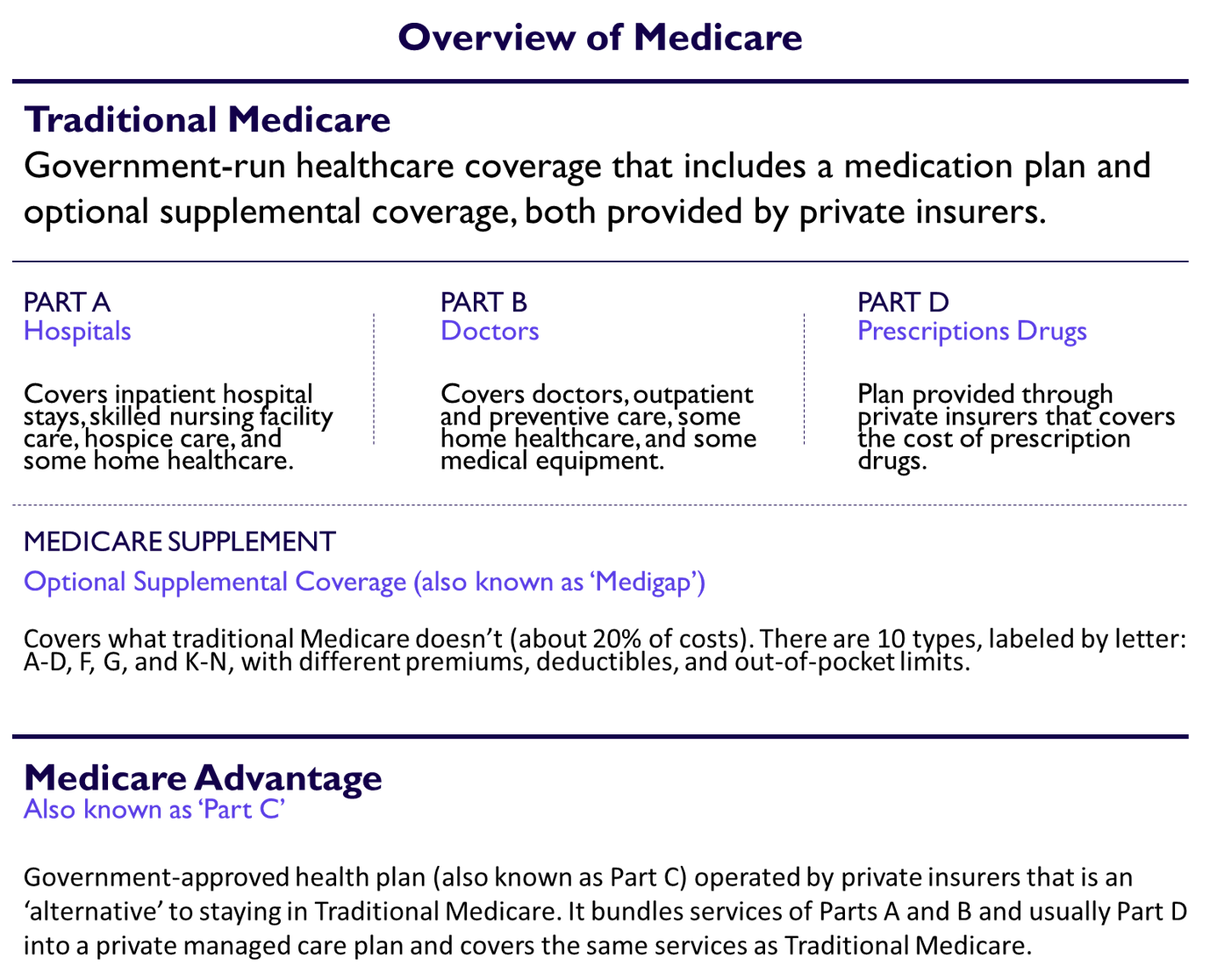

Original Medicare (Part A & B)

Traditionally, Medicare coverage consists of two parts. These are known as ‘Original Medicare’:

Medicare Part A (Hospital Insurance): which covers inpatient hospital care, surgery, lab tests, short-term skilled nursing facilities, home health care as well as hospice care

Medicare Part B (Medical Insurance): which covers medically necessary doctor and outpatient medical services and supplies. Part B also covers ambulance services, durable medical equipment, hospice care, home health care and certain preventive services and screenings

It’s important to understand that Original Medicare does not pay for everything. Even when enrolled in Original Medicare, you are responsible for premiums as well as various out-of-pocket costs such as deductibles, copays, and coinsurance.

Medicare Part C, Part D, and Medicare Supplement

In addition to Original Medicare, there are various other parts of Medicare that are sold by private health insurance companies. These plans often act as:

An alternate to Original Medicare such is the case with Medicare Advantage (also known as Part C coverage); OR

Supplemental coverage that helps to cover some of the out-of-pocket costs that you may need to pay under Original Medicare in return for a monthly premium. These include standalone Prescription Drug Plans (also known as Part D plans) as well as Medicare Supplement plans (also known as ‘Medigap’)

These different parts of Medicare are described in more detail below.

Who is eligible for Medicare?

Medicare eligibility for individuals 65 and over

You are eligible to enroll in Medicare Part A and B if you are:

Over the age 65 and a U.S. citizen; OR

A permanent resident who has been living in the U.S. constantly for the past 5 years

Most people are eligible for premium-free Part A coverage and do not have to pay premiums in order to be covered under Part A. However, for Part B coverage, all Medicare beneficiaries must pay premiums in order to be covered.

The premium for Part B is set by the Centers for Medicare and Medicaid Services (CMS) each year. What you pay will depend on your income filed with the IRS from 2 years ago. In 2026, the standard Part B premium is $202.90 per month for all individuals with income below $109,000 (or $218,000 for those that filed jointly) on their tax return from 2 years ago (2024 tax year).

Eligibility for premium-free Part A

Most people are eligible to receive Part A coverage without needing to pay a premium. If you or your spouse have worked and paid Medicare taxes for at least 10 years (40 quarters) you are eligible to receive premium-free Part A. If you or your spouse did not pay Medicare taxes for this period, you will have to purchase Part A coverage.

Even if you are eligible for premium-free Part A you will still have out-of-pocket costs in the form of deductibles, copays, and coinsurance obligations.

Premiums for Part B (and Part A if applicable) are typically deducted monthly from your Social Security payments. If you do not currently receive Social Security payments but are enrolled in Medicare, you will receive a bill for your premium every 3 months.

Medicare eligibility for individuals under 65

Individuals who are under the age of 65 with disabilities may also qualify for Medicare. These include:

Social Security Disability Benefits: Individuals who have received SSD benefits for at least 24 months

End-Stage Renal Disease (ESRD): Individuals that have ESRD (permanent kidney failure requiring dialysis or transplant). Benefits will typically begin on the first day of the fourth month of dialysis treatments

Amyotrophic Lateral Sclerosis (ALS): Individuals with ALS (also known as Lou Gehrig’s disease). Benefits will typically begin as soon as you start receiving SSD benefits

When can I enroll in Medicare?

Automatic Enrollment

Depending on your current situation you may automatically be enrolled in Medicare:

If you are turning 65 and have been receiving Social Security payments at least 4 months prior to being eligible for Medicare, you will automatically get Part A and B starting the first day of the month you turn 65. If your birthday lands on the first day of the month, then coverage will start the first day of the prior month. You will typically also receive your red, white, and blue Medicare card in the mail 3 months before your 65th birthday

If you are turning 65 and not receiving Social Security: you will need to proactively sign up for Medicare during your Initial Enrollment Period (described below) by contacting the Social Security Administration. This includes anyone who has not been receiving Social Security for at least 4 months prior to being eligible for Medicare

If you are under 65 and have a disability: you will automatically get Part A and B after you have received disability benefits from Social Security Disability Income for 24 months (unless you have ESRD or ALS)

How to Enroll in Medicare

The Social Security Administration (SSA) is in charge of processing enrollment applications for Original Medicare (Part A and B) and overseeing premiums and penalties.

If you are not receiving Social Security and automatically enrolled in Medicare, you can apply for Part A and B coverage through the Social Security Administration website: ssa.gov/benefits/medicare.

Medicare Enrollment Periods

Initial Enrollment Period

If you are turning 65, you have a 7-month ‘Initial Enrollment Period’ to sign up for Part A and/or Part B coverage.

The Initial Enrollment Period begins 3 months before the month you turn 65, includes the month you turn 65 and ends 3 months after the month you turn 65.

If you sign up for Medicare Part A and/or Part B before the month in which you turn 65, your coverage will start on the first day of the month you turn 65 (except if your birthday lands exactly on the first day of the month in which case your coverage starts the first day of the prior month).

Enrolling either in the month of your birthday or after will result in delays in the commencement of coverage by up to 3 months from the date that you sign up.

General Enrollment Period

If you happen to miss your Initial Enrollment Period, you do get another chance to enroll for Medicare Parts A and B between January 1 and March 31 each year (called the ‘General Enrollment Period’). However, if you enroll during this period, your Medicare coverage will begin on the 1st of the month after you apply.

Other Medicare enrollment periods that you should know

There are other ‘enrollment periods’ that you should be aware of once you start receiving Medicare coverage:

Annual Election Period: Every year, Medicare’s annual open enrollment period is October 15 – December 7. During this period, all existing Medicare beneficiaries are allowed to freely switch between different Medicare coverage if they decide to change or update their coverage options.

Special Enrollment Periods: Once you are enrolled in Medicare, most beneficiaries will be unable to switch plans outside of the Annual Election Period unless they experience a ‘qualifying event’. Qualifying events may include things such as a permanent change of address, losing employer coverage or ceasing to work, gaining or losing Medicaid eligibility or if you begin experiencing a severe chronic condition.

When should I enroll in Medicare?

Should I enroll immediately when I turn 65?

If you are turning 65, it is recommended that you enroll in both Medicare Part A and B during your Initial Enrollment Period to avoid any penalties if any of these situations apply to you:

You receive health insurance from you or your spouse’s employer and that employer has fewer than 20 employees

You are currently using COBRA or retiree insurance from a previous job

You are enrolled in individual health insurance plan such as an ACA plan

You rely on short-term insurance, or have no insurance at all

You have VA health coverage

You have TRICARE coverage and are retired

What happens if I’m 65 and still receiving insurance from my employer (or spouse’s employer)?

In general, if the employer providing coverage has 20 or more employees, you can choose to delay your Medicare Part A and B enrollment without any penalties. You may also choose to cancel your employer coverage to use Medicare instead, or have both Medicare and employer coverage at the same time.

For more information on how to manage Medicare alongside employer-provided insurance, refer to our article on Medicare When Working Past 65.

Note that COBRA or other employer-sponsored retiree insurance does not qualify you for Part A and B deferral without penalties. You or your spouse must be working in order to defer enrollment

What happens if I don’t enroll in Medicare when I am eligible?

Medicare Late Enrollment Penalties

If you choose to not enroll in Part A and B when you are first eligible and do not qualify for deferred enrollment, you may be subject to late enrollment penalties when you subsequently decide to enroll in Medicare later. The penalties for delayed enrollment include:

Part A Penalties: If you don’t qualify for premium-free Part A and don’t buy it when you’re first eligible, your monthly premium may go up 10% and you will have to pay the higher premium for twice the number of years you could’ve had Part A, but didn’t sign up

Part B Penalties: If you didn’t get Part B when you were first eligible and did not qualify for deferral, your monthly premium may go up 10% for each 12-month period you could’ve had Part B but didn’t sign up. In most cases, you’ll have to pay this penalty each time you pay your premiums, for as long as you have Part B

What is Medicare Part A, B, C, D, and Medicare Supplement?

Original Medicare

As mentioned at the beginning of this article, traditional Medicare coverage consists of Part A and B coverage and is called ‘Original Medicare’:

Part A (Hospital Insurance):

Part A generally helps pay for care you receive when you are officially admitted as an inpatient to a hospital or skilled nursing facility subsequent to a qualifying hospital stay and for medically necessary purposes. Part A does not cover emergency room visits or situations where you are in the hospital for observation if you are not officially admitted as an ‘inpatient’ – these costs are instead covered under Part B.

If you don’t qualify for premium-free Part A, you can buy Part A and will be required to pay up to $565 each month in 2026. Deductibles, copay and coinsurance out-of-pocket costs will still apply even if you are eligible for premium-free Part A. In 2026, the Part A inpatient hospital deductible that beneficiaries will pay when admitted to the hospital is $1,736 for each benefit period.

Part B (Medical Insurance):

Medicare Part B helps pay for care when you are an outpatient. This could include regular doctor visits, emergency room visits, and most other routine and emergency medical services as well as durable medical equipment, home health care, and some preventive services.

The standard Part B premium amount in 2026 is $202.90 per month. Most people pay the standard Part B premium amount, however, if your income as reported on your IRS tax return from 2 years ago is above $109,000 individually or $218,000 jointly your premium will be higher.

There is a $283 deductible and 20% coinsurance obligation after you reach the deductible.

Medicare Part C, Part D, and Medicare Supplement

In addition to Original Medicare which is provided directly by the federal government, Medicare also includes Part C (Medicare Advantage), Part D (Prescription Drugs Plans), and Medicare Supplement (Medigap) coverage. These are alternate or supplemental coverage options to Original Medicare that are provided by private health insurance companies:

Medicare Part C (Medicare Advantage):

Medicare Advantage is privatized Medicare, which means it’s offered by private health insurance companies that are contracted by the government to deliver Medicare.

Medicare Advantage is a bundled ‘all-in-one’ alternative to Original Medicare and combines everything you get in Part A and B, usually with added benefits like prescription drug coverage, dental, vision, and wellness perks. Medicare Advantage is usually managed care plans (for example, HMO and PPO) and have become more popular because of the additional benefits often included that Original Medicare does not have.

Once you are enrolled in Medicare Advantage, you will be required to use services in accordance with that plan’s policy, such as the use of ‘in-network’ providers to receive care.

Medicare Part D (Prescription Drug Coverage):

Part D refers to prescription drug coverage offered by private health insurance companies and available to everyone who is eligible for Part A or B. Prescription coverage can be purchased as a standalone Prescription Drug Plan (PDP) that is used as supplemental coverage alongside Original Medicare.

Prescription drug coverage can also be accessed via a Medicare Advantage plan that includes prescription drugs as a part of the plan (these are also known as ‘MA-PD’ plans).

Medicare Supplement Insurance (Medigap):

Medigap is supplemental insurance that helps cover “gaps” in Original Medicare and is sold by health private insurance companies. Medigap can only be used with Original Medicare and you can not enroll in a Medigap plan if you are enrolled in a Medicare Advantage plan.

A Medigap policy is designed to help cover out-of-pocket costs (deductibles, copays and coinsurance) that you otherwise may be responsible to pay under Original Medicare in return for a monthly premium.

There are 10 Medigap plans (A, B, C, D, F, G, K, L, M & N) and by law, Medigap plans are standardized. This means Plan G from Company A has exactly the same benefits as Plan G from Company B – therefore your choice comes down to price and the insurer’s reputation

Other Companies Reviewed

5.3

A non-government website that helps customers inquire about different health insurances

Provides both Medicare, ACA and Short Term Medical

Connect people with the right coverage through a data-powered marketplace

Third party reviews and Trustpilot ratings are limited - not strong

6.4

Medicare Supplement (Medigap) - focused service that connects you with brokers based on your information

Medigap.com allows access to different brokers that can provide Medigap quotes

Strong Trustpilot ratings (4.8/5)

Provides only Medicare Supplement/Medigap quotes – no Medicare Advantage or Rx Plans